Due to the existing deployment ban of all overseas Filipino workers (OFW), vacationing OFWs has to secure a clearance from POLO-OWWA to avoid the hassle of missing their flight even they presented an OEC. The ban exempts OFWs who have existing work contracts and those who are going on vacation and returning to the same employers.

Advertisement

Sponsored Links

The clearance is basically a certification that the OFW is an active OWWA member and is currently on a work contract with the same employer.

To get the required clearance, OFWs in Kuwait should go personally to the POLO-OWWA at the Philippine Embassy.

You can at the same time apply for the OEC.

You need to pay KWD8 for your OWWA membership if it is already expired.

You can also apply for the OEC at the POEA should you wish to do so.

While in the Philippines, you need to go to POEA to validate your clearance as well as your OEC if you already have one or you can obtain it from there.

Unvalidated clearance will not be honored at the immigration and could cause problems on your way back to Kuwait.

Unvalidated clearance will not be honored at the immigration and could cause problems on your way back to Kuwait.

|

| OFWs piling up at the Philippine Embassy in Kuwait to secure clearance and OECs. |

Read More:

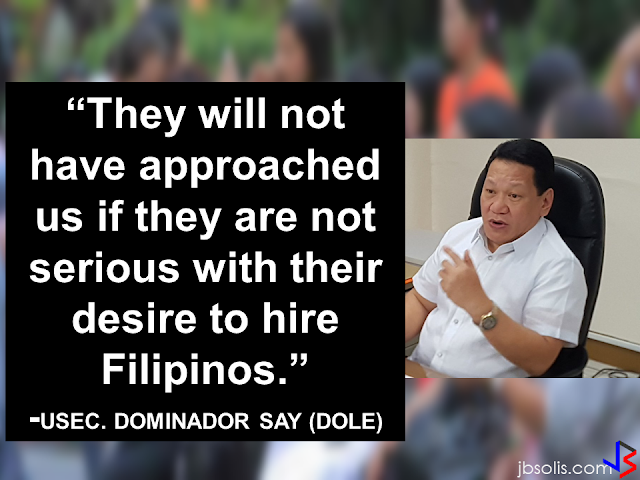

working in Saudi Arabia was killed by an unknown gunman in Cabatuan, Isabela on Sunday. The OFW is in the country to enjoy her vacation and to celebrate her bithday with her loved ones. The victim's mother, Betty Ordonez, said that Jenny Constantino, 29, arrived in the country from Saudi Arabia for a vacation. On Sunday evening, Constantino went out of the house to pick some sweet potato taps just a few steps away from their house at Barangay Calaocan. After a few moments, gunshots were heard and the victims body fell on the ground. The victim suffered multiple gunshot wounds in her body and died while being transported to the nearest hospital. The identity of the gunman is still unknown up to this writing. A female Overseas Filipino Worker (OFW) working in Saudi Arabia was killed by an unknown gunman in Cabatuan, Isabela on Sunday. The OFW is in the country to enjoy her vacation and to celebrate her bithday with her loved ones. The victim's mother, Betty Ordonez, said that Jenny Constantino, 29, arrived in the country from Saudi Arabia for a vacation. On Sunday evening, Constantino went out of the house to pick some sweet potato taps just a few steps away from their house at Barangay Calaocan. After a few moments, gunshots were heard and the victims body fell on the ground. The victim suffered multiple gunshot wounds in her body and died while being transported to the nearest hospital. The identity of the gunman is still unknown up to this writing. According to PRO2 Director Chief Supt. Robert G. Quenery ,the victim was with her niece during the killing and saw he arrival of an unknown gunman on a motorcycle wearing a T-shirt, short pants and a bull cap with face covered with a cloth. the niece was luckily unharmed during the shooting incident. Senior Inspector Prospero Agonoy, Chief of Cabatuan Police, there were no other witnesses aside from the victim's niece \"Advertisements\" The police is now following a trace that will lead to the arrest of the gunman but the details are not disclosed to the public. The family of the OFW is confident that the case will be solved and justice will be served for the killing of their loved one. The brother of the victim appeal to he gunman to surface and admit his crime. The OFW left her 10 years old daughter. Jenny was an OFW for six years and is scheduled to return to Saudi Arabia this coming September \"Sponsored Links\" Read More: China's plans to hire Filipino household workers to their five major cities including Beijing and Shanghai, was reported at a local newspaper Philippine Star. it could be a big break for the household workers who are trying their luck in finding greener pastures by working overseas China is offering up to P100,000 a month, or about HK$15,000. The existing minimum allowable wage for a foreign domestic helper in Hong Kong is around HK$4,310 per month. Dominador Say, undersecretary of the Department of Labor and Employment (DOLE), said that talks are underway with Chinese embassy officials on this possibility. China’s five major cities, including Beijing, Shanghai and Xiamen will soon be the haven for Filipino domestic workers who are seeking higher income. DOLE is expected to have further negotiations on the launch date with a delegation from China in September. according to Usec Say, Chinese employers favor Filipino domestic workers for their English proficiency, which allows them to teach their employers’ children. Chinese embassy officials also mentioned that improving ties with the leadership of President Rodrigo Duterte has paved the way for the new policy to materialize. There is presently a strict work visa system for foreign workers who want to enter mainland China. But according Usec. Say, China is serious about the proposal. Philippine Labor Secretary Silvestre Bello said an estimated 200,000 Filipino domestic helpers are presently working illegally in China. With a great demand for skilled domestic workers, Filipino OFWs would have an option to apply using legal processes on their desired higher salary for their sector. Source: ejinsight.com, PhilStar Read More: The effectivity of the Nationwide Smoking Ban or E.O. 26 (Providing for the Establishment of Smoke-free Environment in Public and Enclosed Places) started today, July 23, but only a few seems to be aware of it. President Rodrigo Duterte signed the Executive Order 26 with the citizens health in mind. Presidential Spokesperson Ernesto Abella said the executive order is a milestone where the government prioritize public health protection. The smoking ban includes smoking in places such as schools, universities and colleges, playgrounds, restaurants and food preparation areas, basketball courts, stairwells, health centers, clinics, public and private hospitals, hotels, malls, elevators, taxis, buses, public utility jeepneys, ships, tricycles, trains, airplanes, and gas stations which are prone to combustion. The Department of Health urges all the establishments to post \"no smoking\" signs in compliance with the new executive order. They also appeal to the public to report any violation against the nationwide ban on smoking in public places. Read More: ©2017 THOUGHTSKOTO www.jbsolis.com SEARCH JBSOLIS, TYPE KEYWORDS and TITLE OF ARTICLE at the box below Smoking is only allowed in designated smoking areas to be provided by the owner of the establishment. Smoking in private vehicles parked in public areas is also prohibited. What Do You Need To know About The Nationwide Smoking Ban Violators will be fined P500 to P10,000, depending on their number of offenses, while owners of establishments caught violating the EO will face a fine of P5,000 or imprisonment of not more than 30 days. The Department of Health urges all the establishments to post \"no smoking\" signs in compliance with the new executive order. They also appeal to the public to report any violation against the nationwide ban on smoking in public places. ©2017 THOUGHTSKOTO Dominador Say, undersecretary of the Department of Labor and Employment (DOLE), said that talks are underway with Chinese embassy officials on this possibility. China’s five major cities, including Beijing, Shanghai and Xiamen will soon be the destination for Filipino domestic workers who are seeking higher income. ©2017 THOUGHTSKOTO www.jbsolis.com SEARCH JBSOLIS, TYPE KEYWORDS and TITLE OF ARTICLE at the box below According to PRO2 Director Chief Supt. Robert G. Quenery ,the victim was with her niece during the killing and saw he arrival of an unknown gunman on a motorcycle wearing a T-shirt, short pants and a bull cap with face covered with a cloth. the niece was luckily unharmed during the shooting incident. Senior Inspector Prospero Agonoy, Chief of Cabatuan Police, there were no other witnesses aside from the victim's niece \"Advertisements\" A female Overseas Filipino Worker (OFW) working in Saudi Arabia was killed by an unknown gunman in Cabatuan, Isabela on Sunday. The OFW is in the country to enjoy her vacation and to celebrate her bithday with her loved ones. The victim's mother, Betty Ordonez, said that Jenny Constantino, 29, arrived in the country from Saudi Arabia for a vacation. On Sunday evening, Constantino went out of the house to pick some sweet potato taps just a few steps away from their house at Barangay Calaocan. After a few moments, gunshots were heard and the victims body fell on the ground. The victim suffered multiple gunshot wounds in her body and died while being transported to the nearest hospital. The identity of the gunman is still unknown up to this writing. According to PRO2 Director Chief Supt. Robert G. Quenery ,the victim was with her niece during the killing and saw he arrival of an unknown gunman on a motorcycle wearing a T-shirt, short pants and a bull cap with face covered with a cloth. the niece was luckily unharmed during the shooting incident. Senior Inspector Prospero Agonoy, Chief of Cabatuan Police, there were no other witnesses aside from the victim's niece \"Advertisements\" The police is now following a trace that will lead to the arrest of the gunman but the details are not disclosed to the public. The family of the OFW is confident that the case will be solved and justice will be served for the killing of their loved one. The brother of the victim appeal to he gunman to surface and admit his crime. The OFW left her 10 years old daughter. Jenny was an OFW for six years and is scheduled to return to Saudi Arabia this coming September \"Sponsored Links\" Read More: China's plans to hire Filipino household workers to their five major cities including Beijing and Shanghai, was reported at a local newspaper Philippine Star. it could be a big break for the household workers who are trying their luck in finding greener pastures by working overseas China is offering up to P100,000 a month, or about HK$15,000. The existing minimum allowable wage for a foreign domestic helper in Hong Kong is around HK$4,310 per month. Dominador Say, undersecretary of the Department of Labor and Employment (DOLE), said that talks are underway with Chinese embassy officials on this possibility. China’s five major cities, including Beijing, Shanghai and Xiamen will soon be the haven for Filipino domestic workers who are seeking higher income. DOLE is expected to have further negotiations on the launch date with a delegation from China in September. according to Usec Say, Chinese employers favor Filipino domestic workers for their English proficiency, which allows them to teach their employers’ children. Chinese embassy officials also mentioned that improving ties with the leadership of President Rodrigo Duterte has paved the way for the new policy to materialize. There is presently a strict work visa system for foreign workers who want to enter mainland China. But according Usec. Say, China is serious about the proposal. Philippine Labor Secretary Silvestre Bello said an estimated 200,000 Filipino domestic helpers are presently working illegally in China. With a great demand for skilled domestic workers, Filipino OFWs would have an option to apply using legal processes on their desired higher salary for their sector. Source: ejinsight.com, PhilStar Read More: The effectivity of the Nationwide Smoking Ban or E.O. 26 (Providing for the Establishment of Smoke-free Environment in Public and Enclosed Places) started today, July 23, but only a few seems to be aware of it. President Rodrigo Duterte signed the Executive Order 26 with the citizens health in mind. Presidential Spokesperson Ernesto Abella said the executive order is a milestone where the government prioritize public health protection. The smoking ban includes smoking in places such as schools, universities and colleges, playgrounds, restaurants and food preparation areas, basketball courts, stairwells, health centers, clinics, public and private hospitals, hotels, malls, elevators, taxis, buses, public utility jeepneys, ships, tricycles, trains, airplanes, and gas stations which are prone to combustion. The Department of Health urges all the establishments to post \"no smoking\" signs in compliance with the new executive order. They also appeal to the public to report any violation against the nationwide ban on smoking in public places. Read More: ©2017 THOUGHTSKOTO www.jbsolis.com SEARCH JBSOLIS, TYPE KEYWORDS and TITLE OF ARTICLE at the box below Smoking is only allowed in designated smoking areas to be provided by the owner of the establishment. Smoking in private vehicles parked in public areas is also prohibited. What Do You Need To know About The Nationwide Smoking Ban Violators will be fined P500 to P10,000, depending on their number of offenses, while owners of establishments caught violating the EO will face a fine of P5,000 or imprisonment of not more than 30 days. The Department of Health urges all the establishments to post \"no smoking\" signs in compliance with the new executive order. They also appeal to the public to report any violation against the nationwide ban on smoking in public places. ©2017 THOUGHTSKOTO Dominador Say, undersecretary of the Department of Labor and Employment (DOLE), said that talks are underway with Chinese embassy officials on this possibility. China’s five major cities, including Beijing, Shanghai and Xiamen will soon be the destination for Filipino domestic workers who are seeking higher income. ©2017 THOUGHTSKOTO www.jbsolis.com SEARCH JBSOLIS, TYPE KEYWORDS and TITLE OF ARTICLE at the box below The police is now following a trace that will lead to the arrest of the gunman but the details are not disclosed to the public. The family of the OFW is confident that the case will be solved and justice will be served for the killing of their loved one. The brother of the victim appeal to he gunman to surface and admit his crime. The OFW left her 10 years old daughter. Jenny was an OFW for six years and is scheduled to return to Saudi Arabia this coming September. Source: ABS-CBN News \"Sponsored Links\" Read More: China's plans to hire Filipino household workers to their five major cities including Beijing and Shanghai, was reported at a local newspaper Philippine Star. it could be a big break for the household workers who are trying their luck in finding greener pastures by working overseas China is offering up to P100,000 a month, or about HK$15,000. The existing minimum allowable wage for a foreign domestic helper in Hong Kong is around HK$4,310 per month. Dominador Say, undersecretary of the Department of Labor and Employment (DOLE), said that talks are underway with Chinese embassy officials on this possibility. China’s five major cities, including Beijing, Shanghai and Xiamen will soon be the haven for Filipino domestic workers who are seeking higher income. DOLE is expected to have further negotiations on the launch date with a delegation from China in September. according to Usec Say, Chinese employers favor Filipino domestic workers for their English proficiency, which allows them to teach their employers’ children. Chinese embassy officials also mentioned that improving ties with the leadership of President Rodrigo Duterte has paved the way for the new policy to materialize. There is presently a strict work visa system for foreign workers who want to enter mainland China. But according Usec. Say, China is serious about the proposal. Philippine Labor Secretary Silvestre Bello said an estimated 200,000 Filipino domestic helpers are presently working illegally in China. With a great demand for skilled domestic workers, Filipino OFWs would have an option to apply using legal processes on their desired higher salary for their sector. Source: ejinsight.com, PhilStar Read More: The effectivity of the Nationwide Smoking Ban or E.O. 26 (Providing for the Establishment of Smoke-free Environment in Public and Enclosed Places) started today, July 23, but only a few seems to be aware of it. President Rodrigo Duterte signed the Executive Order 26 with the citizens health in mind. Presidential Spokesperson Ernesto Abella said the executive order is a milestone where the government prioritize public health protection. The smoking ban includes smoking in places such as schools, universities and colleges, playgrounds, restaurants and food preparation areas, basketball courts, stairwells, health centers, clinics, public and private hospitals, hotels, malls, elevators, taxis, buses, public utility jeepneys, ships, tricycles, trains, airplanes, and gas stations which are prone to combustion. The Department of Health urges all the establishments to post \"no smoking\" signs in compliance with the new executive order. They also appeal to the public to report any violation against the nationwide ban on smoking in public places. Read More: ©2017 THOUGHTSKOTO www.jbsolis.com SEARCH JBSOLIS, TYPE KEYWORDS and TITLE OF ARTICLE at the box below Smoking is only allowed in designated smoking areas to be provided by the owner of the establishment. Smoking in private vehicles parked in public areas is also prohibited. What Do You Need To know About The Nationwide Smoking Ban Violators will be fined P500 to P10,000, depending on their number of offenses, while owners of establishments caught violating the EO will face a fine of P5,000 or imprisonment of not more than 30 days. The Department of Health urges all the establishments to post \"no smoking\" signs in compliance with the new executive order. They also appeal to the public to report any violation against the nationwide ban on smoking in public places. ©2017 THOUGHTSKOTO Dominador Say, undersecretary of the Department of Labor and Employment (DOLE), said that talks are underway with Chinese embassy officials on this possibility. China’s five major cities, including Beijing, Shanghai and Xiamen will soon be the destination for Filipino domestic workers who are seeking higher income. ©2017 THOUGHTSKOTO www.jbsolis.com SEARCH JBSOLIS, TYPE KEYWORDS and TITLE OF ARTICLE at the box below")